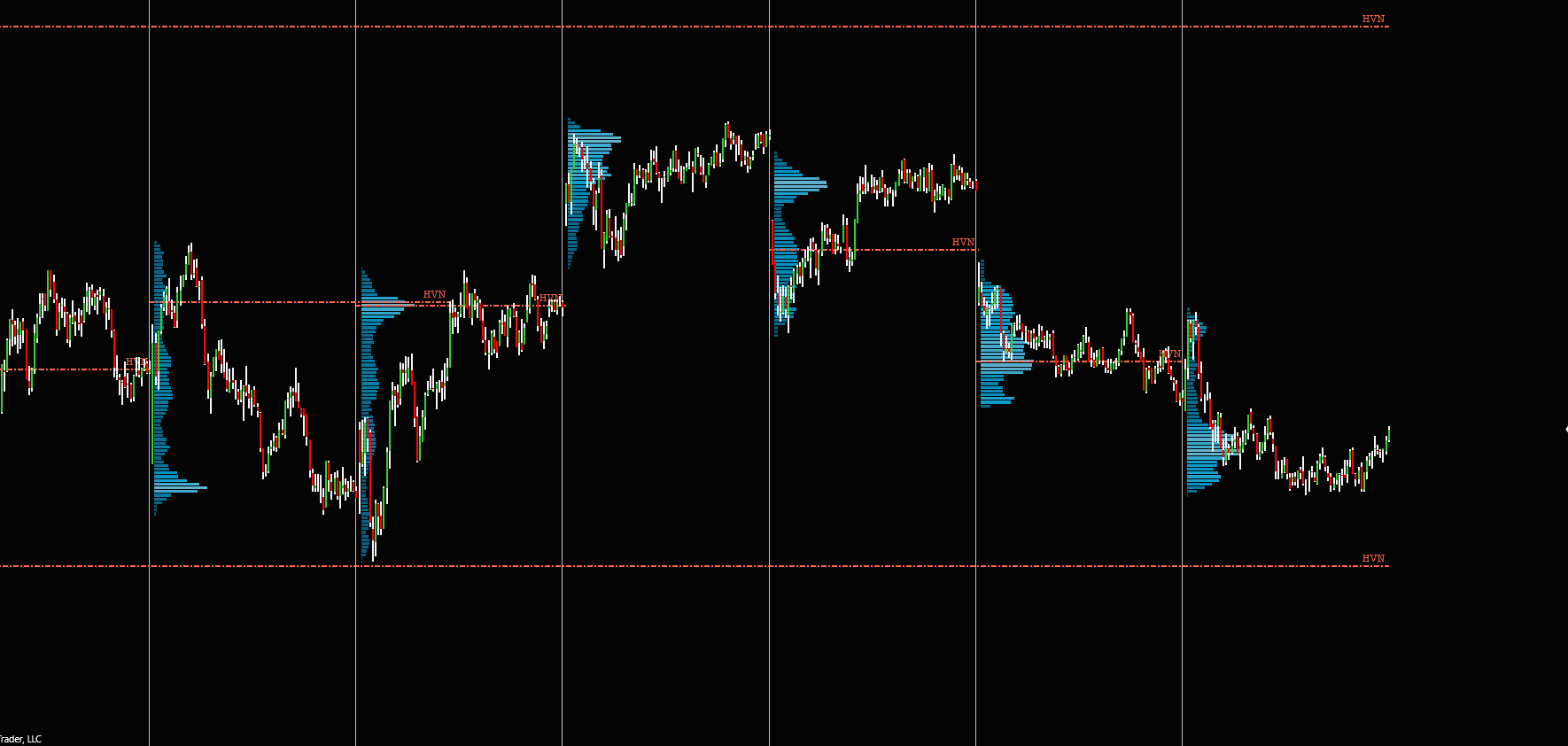

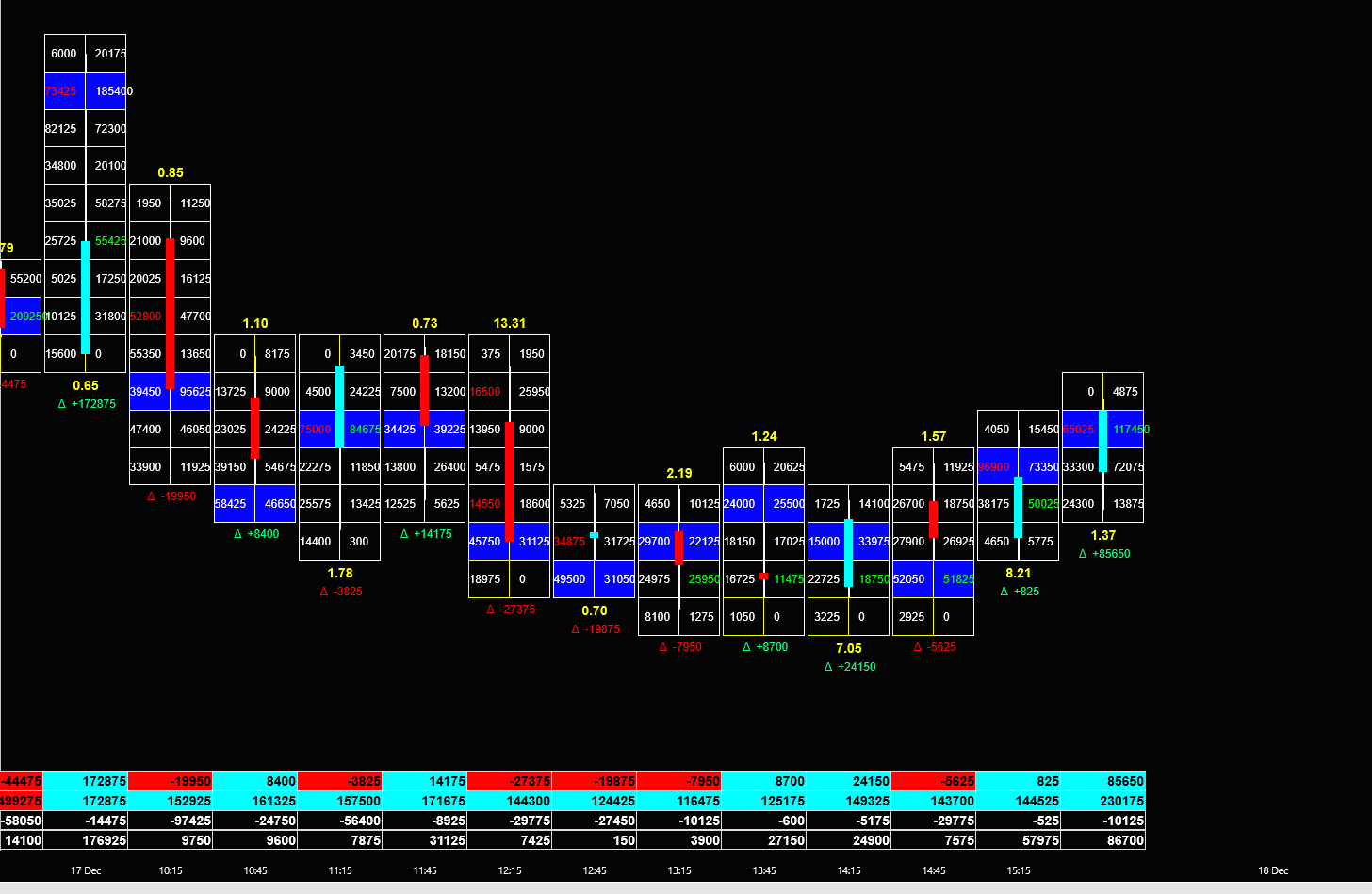

The Nifty 50 witnessed a volatile trading session on 17 December 2025, showing early signs of strength but failing to hold higher levels by the close. Although the market opened firm, it ended the day with mild losses, hinting at selling pressure and weak global cues.

Nifty Overview

- Opening: 25,902.40 (Gap down by 42.30 points)

- Day’s High: 25,929.15

- Day’s Low: 25,770.35

- Closing: 25,818.55

- Net Change: -41.55 points (-0.16%)

- India VIX: Dropped by 2.19%

The index opened near 25,900 and briefly crossed above this mark in the first 15 minutes, trapping intraday bulls. Despite early optimism, global market weakness and USD/INR pressure didn’t support the upward movement. As a result, the Nifty slipped nearly 100 points from the intraday high before stabilizing near the 25,800 zone.

Market Behavior

Today’s session was defined by early bullish momentum followed by sustained selling. The 25,900–26,000 zone acted as a strong resistance area, where many traders seemed to get trapped in long positions. Although some expected 25,800 to provide strong support, continued selling pressure suggests otherwise.

The positive aspect, however, is the market’s stability — it wasn’t a crash day. Instead, it was a consolidation session, indicating that traders are waiting for fresh triggers from global developments or policy comments.

Technical and Sentimental Overview

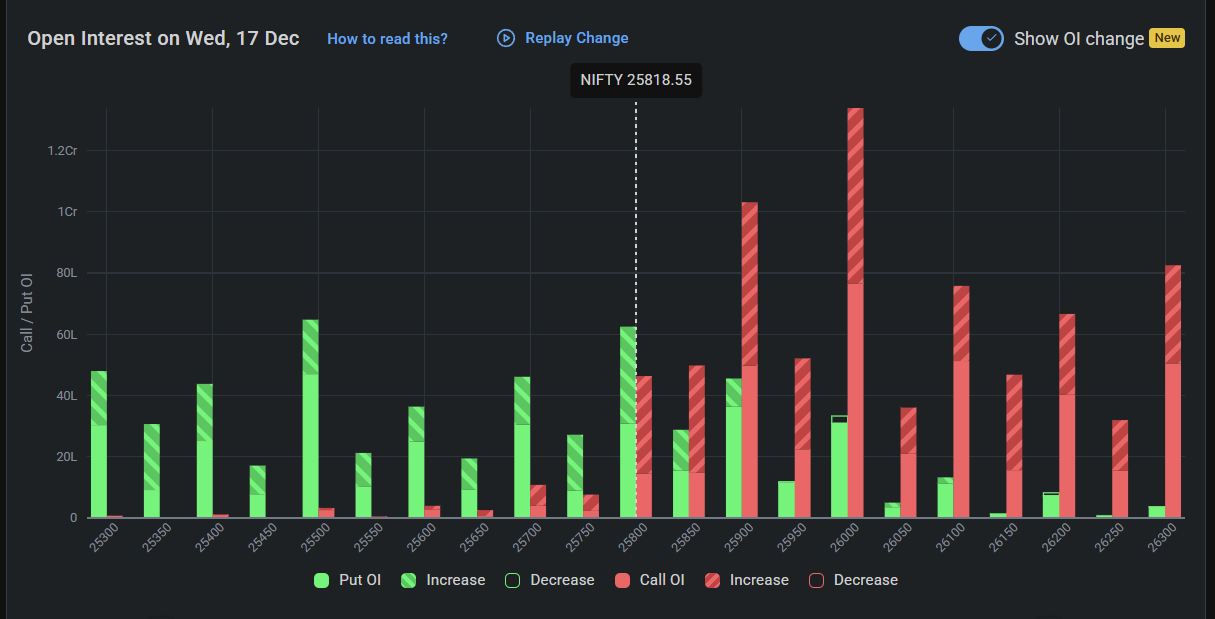

- Key Levels to Watch: 26,000 (Resistance) and 25,800 (Support)

- Overall Sentiment: Bearish to neutral

- OI Data:

- Highest Call OI: 26,000 strike – indicating strong resistance

- Highest Put OI: 25,800 strike – showing limited downside protection

The data clearly shows the index trapped between strong call writing at 26,000 and put writing at 25,800. If selling continues, the put writers might unwind, paving the way for more downside in the near term.

Sectoral Performance

- Top Gainer: PSU Banks – showing relative strength despite broader market weakness

- Top Loser: Consumer Sector – under pressure due to weak demand outlook and stretched valuations

This sectoral divergence suggests that value buying in PSU banks continued, while profit booking hit FMCG and consumer names.

Major Global and Domestic News

- RBI governor signals that interest rates will remain low for a long period, as reported by FT.

- RBI intervenes decisively to stabilize the rupee’s decline against the U.S. dollar.

- India’s trade standoff with the U.S. continues to keep the rupee under pressure.

These developments influenced traders’ sentiment. The rupee’s weakness likely weighed on foreign investor confidence, triggering mild FII outflows and reinforcing the bearish undertone in equity indices.

Why Is the Market Falling Continuously?

The recent fall in the market can be attributed to several technical and macro factors:

- Global Market Sell-Off: Weakness in U.S. and Asian markets has increased risk aversion.

- Rupee Depreciation: A weaker rupee often triggers FII selling in equity markets.

- Profit Booking on Highs: After strong rallies earlier this month, traders are reducing exposure.

- Lack of Domestic Triggers: With limited earnings updates or fresh policy announcements, the market is following global cues.

- Higher U.S. Yields: Rising yields in global bond markets have reduced appetite for risk assets.

However, the decline isn’t panic-driven. The market seems to be digesting earlier gains and finding short-term stability before its next major move.

Final Thoughts

The Nifty remains under pressure, trading below the key 26,000 resistance zone. Traders should stay cautious, watch global cues, and track RBI actions closely as policymakers attempt to strengthen the rupee. A decisive move above 26,000 could shift sentiment, while a break below 25,800 might trigger further downside momentum.

Disclaimer

I am not a SEBI-registered advisor. This analysis is purely for educational purposes. Financial markets involve risk; please consult your financial advisor before making investment decisions. I am not affiliated with any broker or trading platform. The charts and statements shared are intended for transparency and learning — not for promotion or recommendation

Comments are closed