Nifty witnessed another sharp decline on 8 December 2025, slipping below the crucial 26,000 mark amid weak global cues and continuous foreign fund outflows. Rising US 10-year bond yields, a stronger US Dollar Index, surging USD/INR, and a sudden spike in crude oil prices over the weekend dented investor sentiment.

Foreign Institutional Investors (FIIs) continued to offload their positions as global risk sentiment turned cautious. The combination of rising yields, a weakening rupee, and higher crude oil prices created pressure across sectors and kept Indian equities in the red throughout the session.

Market Summary

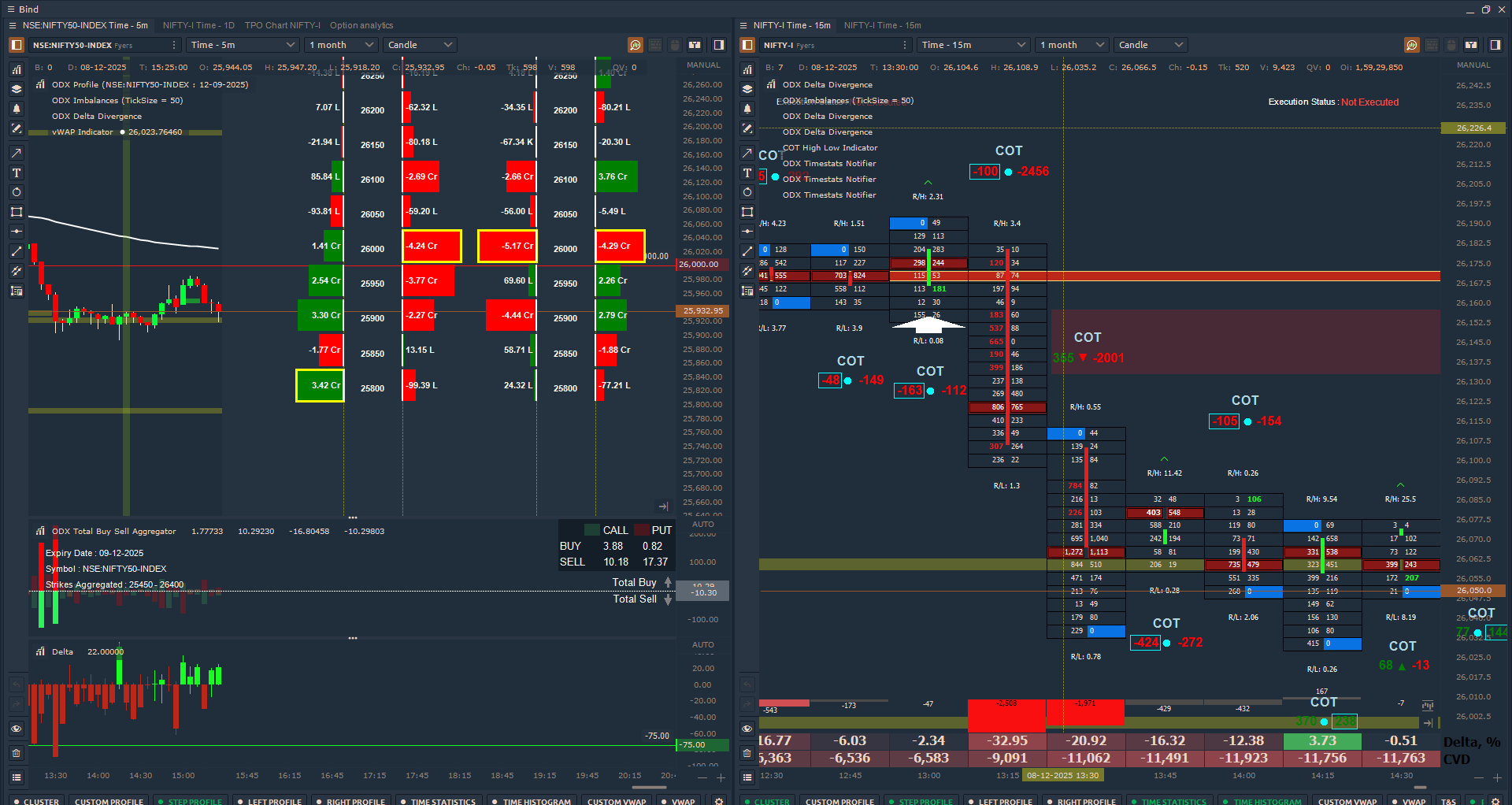

- Nifty opened gap down by 26.65 points at 26,159.80, made an intraday high of 26,178.70, a low of 25,892.25, and finally closed at 25,960.55 — down by 225.90 points (-0.86%).

- India VIX surged by 7.85% to 11.13, signaling rising market nervousness and expectations of higher volatility ahead.

In the initial 5 minutes, the negative delta percentage stood at 35.25%, reflecting strong selling pressure. Nifty broke below the Value Area Low (VAL) early in the session, and despite brief attempts to hold at 26,100, the level failed to provide support. Subsequently, 26,000 also gave way, triggering further downside towards 25,900.

Towards the end, Nifty recovered by about 50–60 points, but the bias remained negative. Lately, it has become increasingly difficult to form a stable short-term directional view due to heightened volatility and inconsistent global cues.

Bonus Point – Volatility Warning

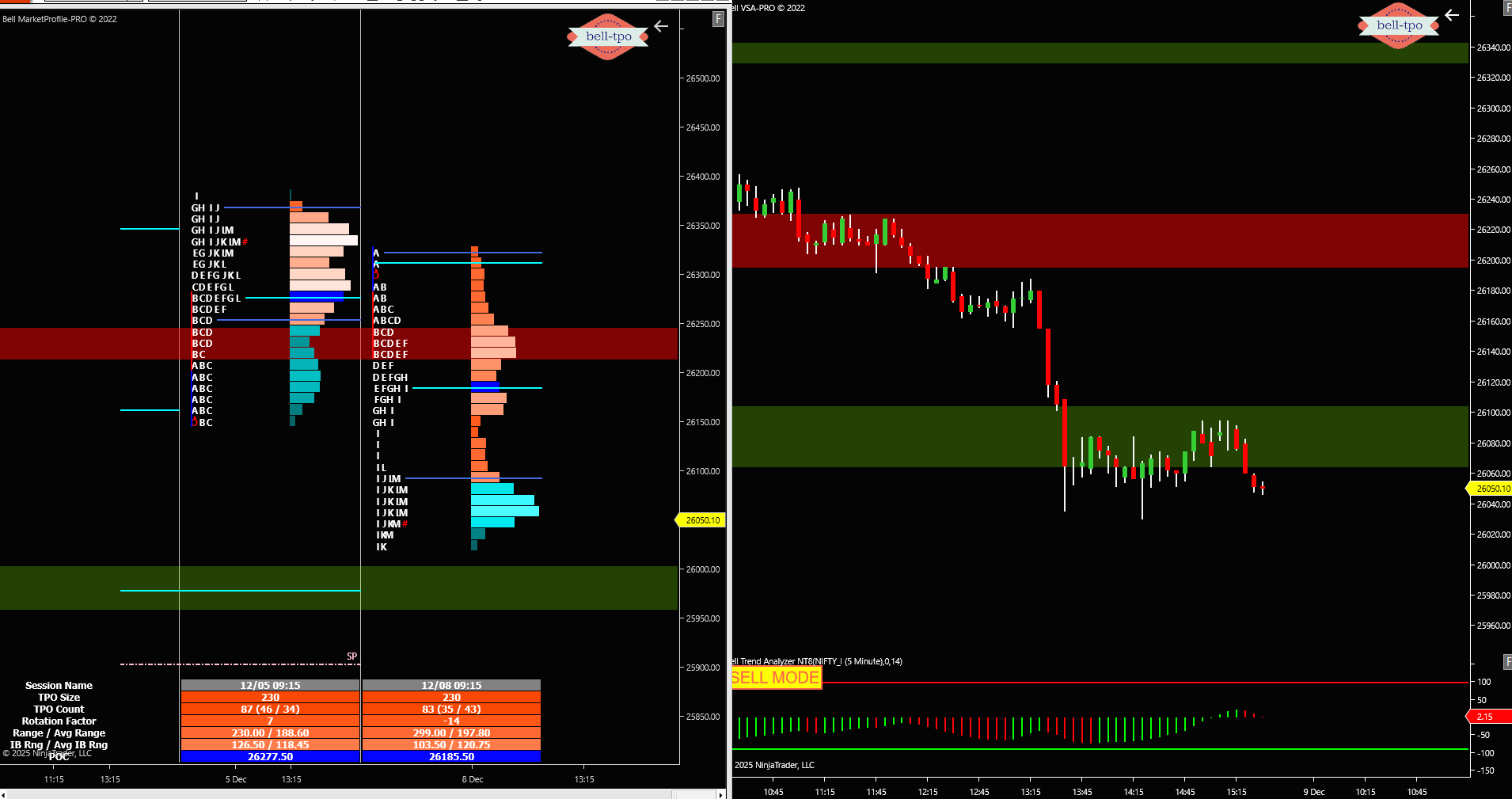

Today’s jump in the VIX by 7.85% is a clear warning for options traders. Such a sudden rise can result in premium erosion once volatility collapses, especially for short-term option buyers. Additionally, today’s rotation factor reading of -14 indicates heavy selling pressure, reinforcing a bearish undertone.

Traders should stay cautious as the market is in a sensitive phase where volatility spikes and global macro triggers can cause sharp intraday swings.

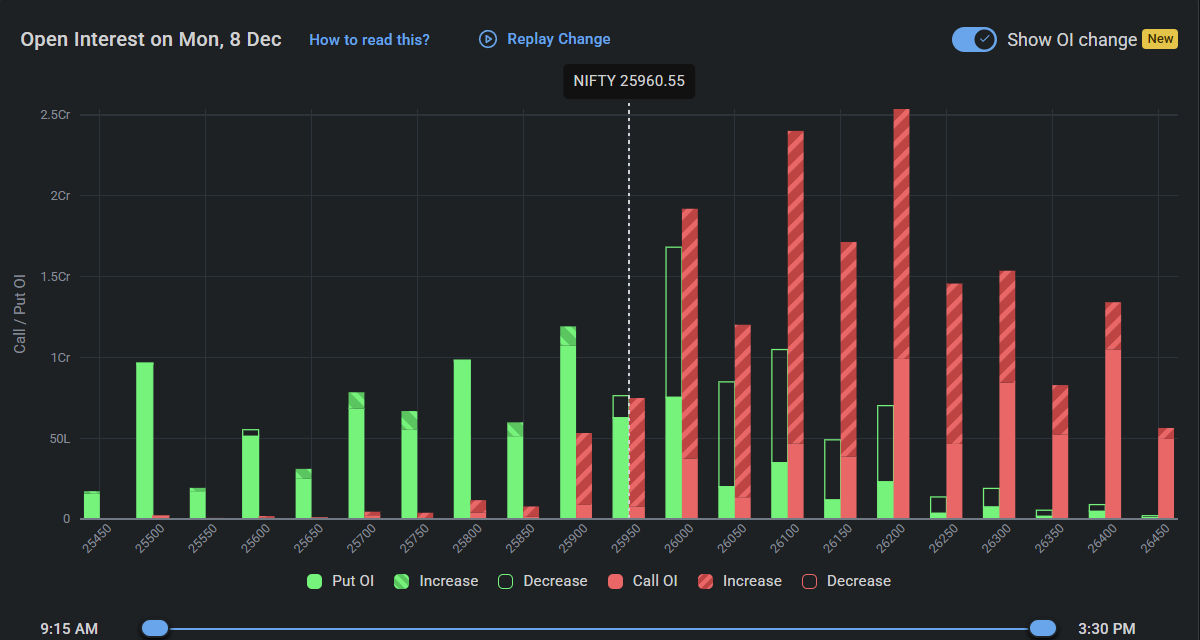

Open Interest (OI) Analysis – December 9 Expiry

- Highest Call OI: 26,200

- Highest Put OI: 25,900

- Significant OI Change:

- Call OI increased at 26,200, indicating rising resistance at that level.

- Put OI decreased at 26,000, suggesting weakening support.

This OI positioning shows a clear bearish bias, with traders expecting resistance near 26,200 and limited downside protection until 25,900.

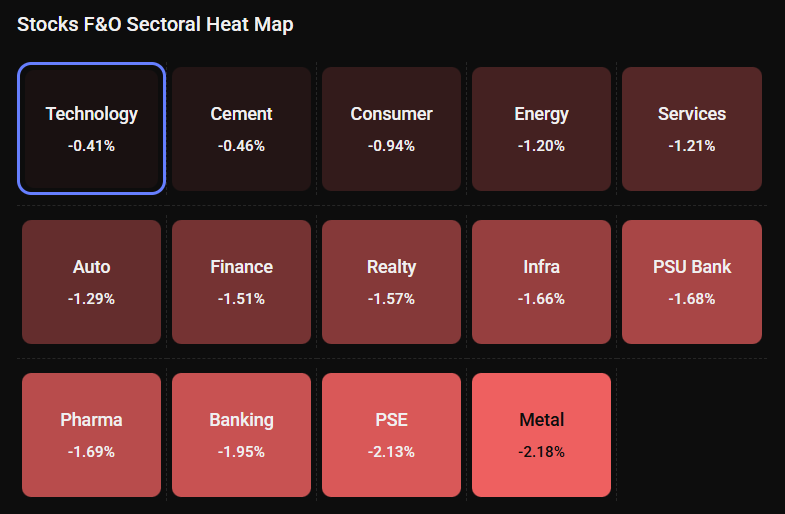

Sectoral Performance

All major sectoral indices ended in negative territory, with metal stocks leading the decline. The combined effect of weak global demand outlook and rising dollar index weighed heavily on commodity-related sectors. Banking, IT, and auto stocks also faced mild to moderate pressure.

Global Market Cues

- Rupee weakened alongside local equities amid a stronger US Dollar and rising US bond yields.

- Gold prices gained, supported by expectations of a possible Fed rate cut early next year and a slightly softer US Dollar.

- Investors are also tracking US-India trade talks and the upcoming Federal Reserve rate decision, both of which may significantly influence market direction in the near term.

Overall, the global environment currently remains unsupportive for Indian equities, leading to persistent FII outflows and subdued investor sentiment.

Disclaimer

This analysis is for educational purposes only. The author is not a SEBI-registered advisor. The stock market involves risks—please consult your financial advisor before making any investment or trading decisions.

All shared content reflects personal study and opinion. No platforms or products mentioned are promoted or affiliated. The intent is purely educational—to spread awareness and demystify options trading as a risk-management tool.

Comments are closed