Market summary

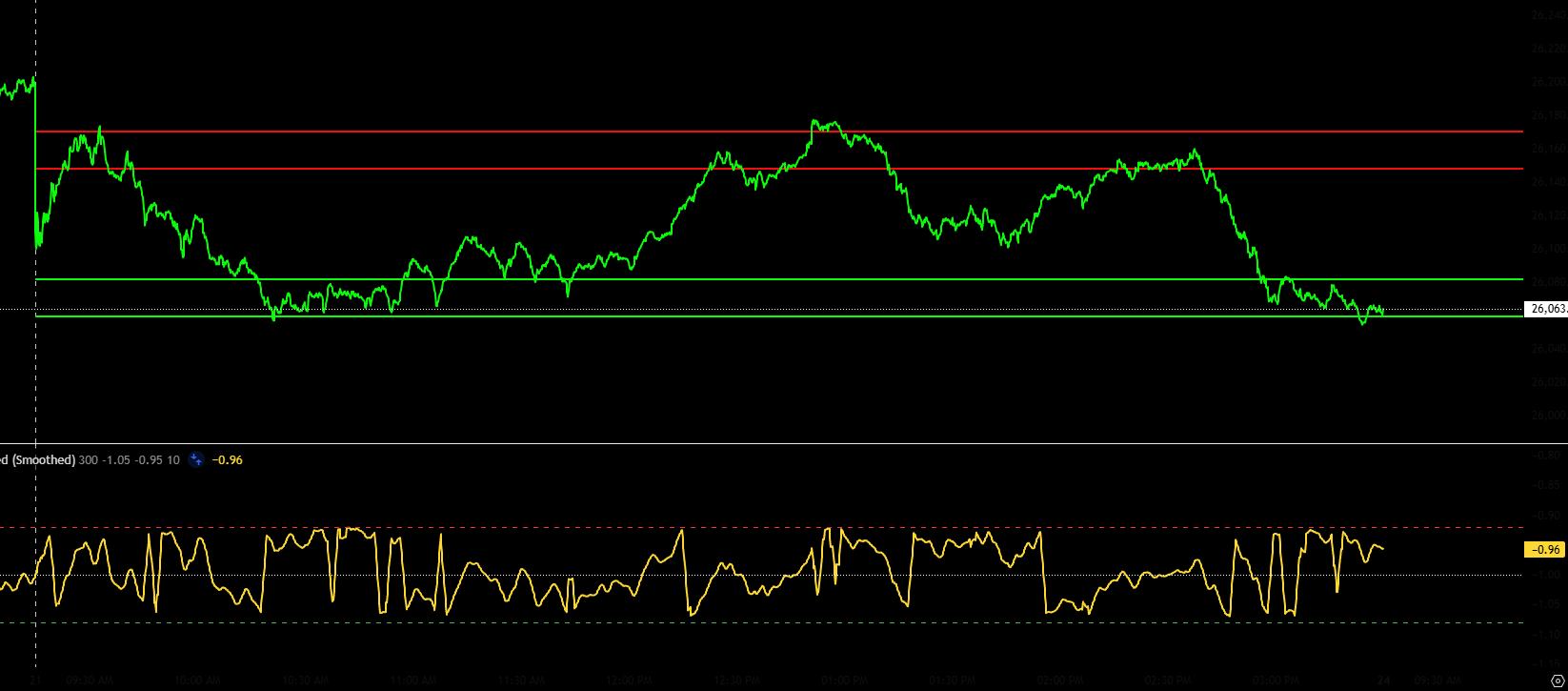

Nifty opened with a gap down of 82.60 points at 26,109.55, tested a high of 26,179.20, a low of 26,052.20 and finally closed at 26,068.15, down 124 points or around −0.47% for the day. Price action in the first few minutes showed buyers trying to defend the 26,100 area, but sellers quickly regained control, pushing the index to spend most of the session oscillating between 26,000 and 26,100.

The key takeaway is that despite heavy global risk-off sentiment, Nifty absorbed selling pressure and protected the 26,000 put writers’ zone, indicating that genuine trend reversal will only be confirmed on a sustained close below 26,000. India VIX jumped by about 12.27% to 13.63, signalling that traders are aggressively repricing risk and that volatility is likely to play a major role into the next expiry.

Why the market fell today

The decline was primarily driven by weak global cues as Asian and US markets turned risk-off, with traders booking profits after recent highs and reacting to renewed uncertainty around global growth and US interest-rate expectations. Domestically, sentiment was hit by flash PMI data showing that India’s November business activity slowed to a six‑month low, with manufacturing at a nine‑month low, signalling loss of momentum in the real economy.

On the macro side, the Indian rupee logged its steepest single‑day fall in more than three months and briefly breached the 89.50 per US dollar mark, closing around 89.46, which typically pressures foreign investor sentiment and raises concerns on imported inflation. Together, slower PMI data, a record‑weak rupee and global equity weakness created a risk‑off environment, leading to broad‑based selling across major sectors and pushing Nifty lower despite intraday attempts to bounce.

Volatility and VIX – bonus point

India VIX’s sharp rise of 12.27% to around 13.63 reflects a quick repricing of option premiums and expectations of wider intraday swings in the coming sessions. For option traders, this means both opportunity and risk: option buyers get better payoff potential, while option sellers must be more selective, size positions carefully and respect stop‑losses as mark‑to‑market swings can expand sharply near expiry.

Into the next expiry, elevated VIX suggests that even if headline indices appear range‑bound, intraday volatility spikes and sharp reversals can be frequent, making risk management and position hedging more important than pure direction calls.

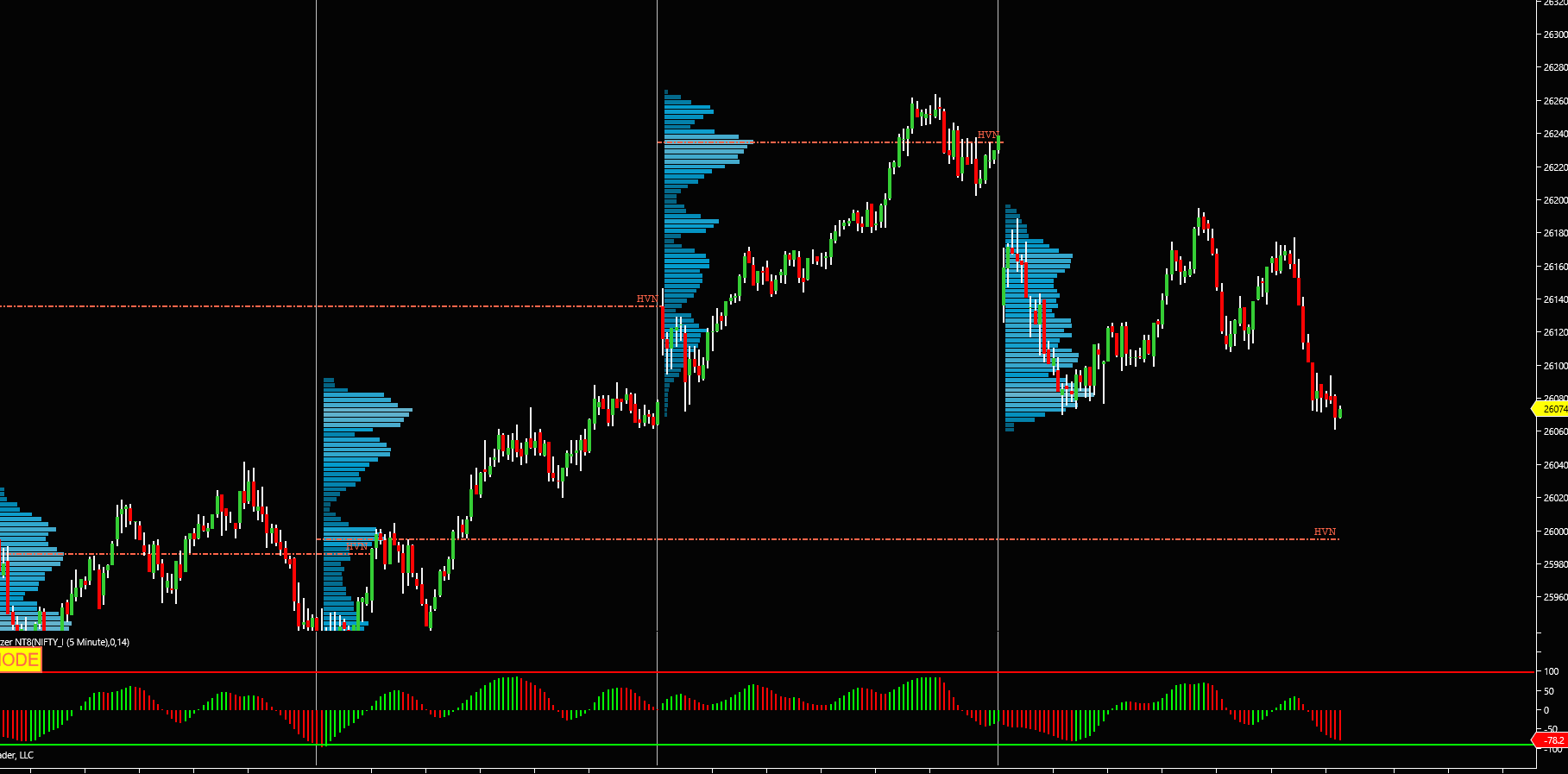

Technical view – Nifty levels

Today’s Point of Control (POC) around 26,050 shows that maximum volume and time were spent near this level, marking it as an important intraday reference for bulls and bears. Rotation factor near 1 indicates a relatively balanced but nervous session, with repeated tests of intraday levels rather than a one‑way trending day.

Immediate support remains at 26,000, which also coincides with the largest put open interest, while resistance is seen near 26,200 where both price supply and heavy call writing are visible. As long as Nifty trades above 26,000 on closing basis, the broader structure can still be interpreted as a high‑level consolidation rather than a confirmed downtrend, but a decisive close below 26,000 would open up deeper downside and justify a more clearly bearish view.

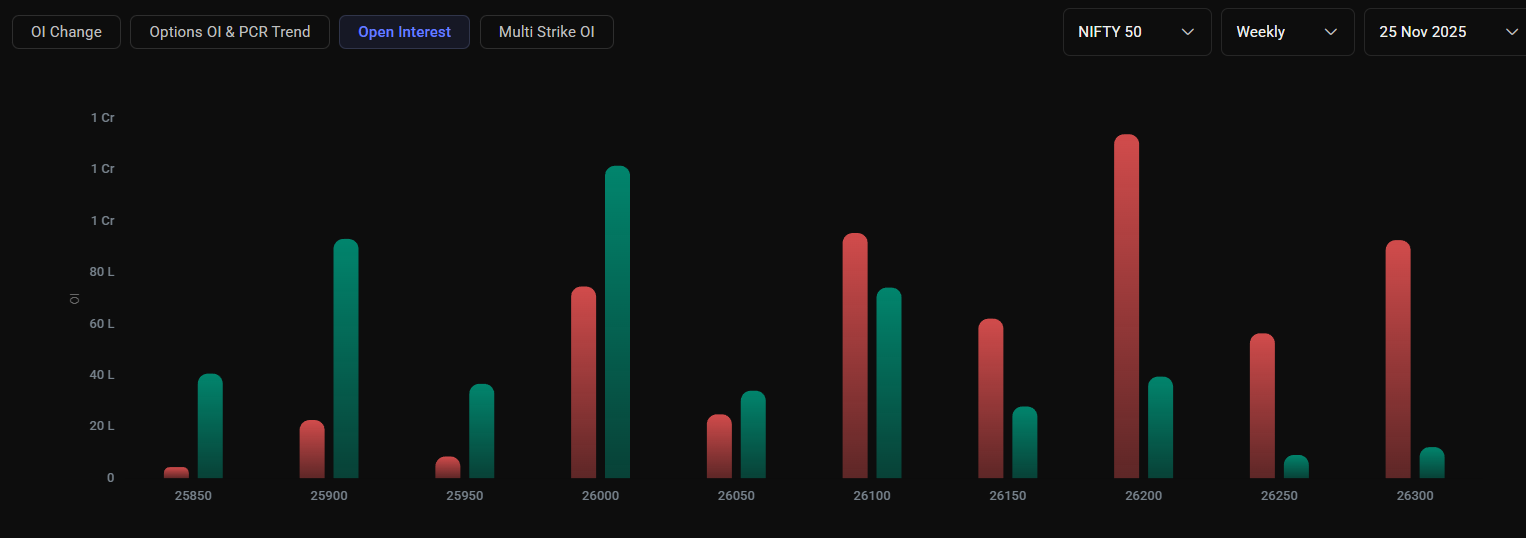

Open interest for 25 November expiry

For the upcoming 25 November expiry, call open interest is highest at 26,200, while put open interest is highest at 26,000, creating a tight 200‑point expiry range where option writers currently have maximum exposure. The largest change in OI today came from call writing at 26,200, whereas put OI did not see any significant fresh addition at lower strikes, suggesting that traders are more comfortable capping upside than aggressively defending new downside levels for this expiry.

This structure indicates a short‑term ceiling near 26,200 and a key battle zone at 26,000; a move and close beyond either side, particularly with follow‑through OI shift, can trigger short covering or long liquidation waves into expiry.

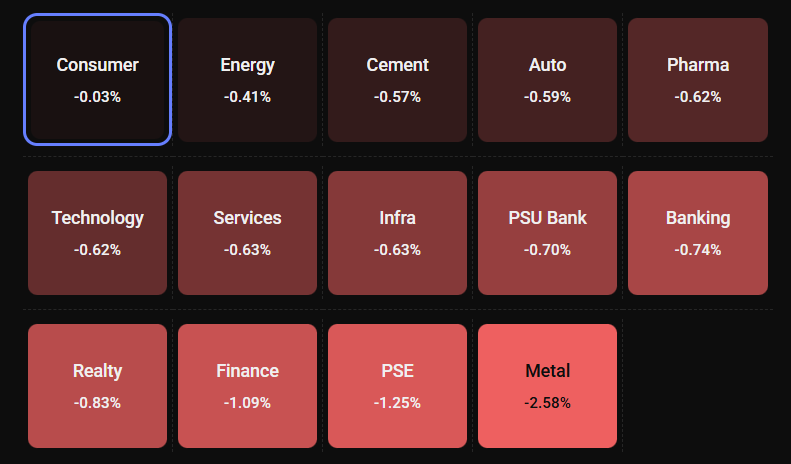

Sectoral movement

All major sectoral indices ended in the red, reflecting broad‑based selling rather than a move limited to a single theme or pocket. Cyclical and rate‑sensitive sectors were particularly hit as concerns about global growth, currency weakness and risk‑off sentiment drove traders to reduce leveraged and high‑beta exposure.

Such a market‑wide decline typically signals sentiment‑driven risk reduction rather than stock‑specific issues, which also aligns with the impact from macro data and currency moves seen today.

Global and domestic macro news

Fresh PMI data showed that India’s November business growth slipped to a six‑month low, with the flash Composite PMI easing to around 59.9 and manufacturing PMI dropping to a nine‑month low near 57.4, pointing to softer factory output and weaker new orders. While the readings remain well above the 50 threshold that separates expansion from contraction, the third straight monthly decline in PMI suggests that the pace of expansion is moderating.

At the same time, the Indian rupee suffered its steepest single‑day fall in over three months, breaching the 89 per US dollar mark intraday and closing near a record low around 89.46–89.48, pressuring importers and raising concern about external stability. This combination of slower PMI momentum and a record‑weak rupee added to global risk‑off cues from US and Asian markets, amplifying selling pressure on domestic equities.

Additional professional insights

From an order‑flow perspective, the fact that Nifty repeatedly bounced from just above 26,000 despite strong global and currency headwinds suggests that responsive buyers and short‑covering activity are active around this level, likely influenced by heavy put writing and institutional hedging flows. However, the lack of aggressive put addition at lower strikes and the build‑up of call OI at 26,200 indicate that smart money is still cautious on upside, preferring to monetize volatility and cap rallies rather than chase breakouts.

For positional traders, the market appears to be in a “volatility‑within‑range” phase: structurally positive above 26,000, but tactically vulnerable to negative global news, rupee weakness and further deterioration in manufacturing data. In such an environment, defined‑risk option strategies like spreads, limited‑risk straddles/strangles or iron condors around the 26,000–26,200 band can be more suitable than naked option selling, especially with VIX elevated and macro data‑driven gaps becoming more frequent.

Disclaimer

This analysis is for educational and informational purposes only and is not registered investment advice; equity and derivatives markets involve significant risk, and readers should consult their SEBI‑registered investment adviser before making any investment or trading decisions. There is no association or endorsement with any broker, trading platform or product mentioned or shown, and any P&L or examples discussed are purely to share learning and help demystify options, not to sell courses or guarantee any outcome.

Comments are closed