On August 8, 2025, the Indian equity markets faced a sharp downturn with the Nifty closing 232.85 points lower (-0.95%) at 24,363.30, sliding after a gap-down open. The day was dominated by strong selling pressure, rising volatility, and a broad sectoral decline amid escalating global tensions and US tariff impacts on key Indian export sectors.

Market Opening and Intraday Movement

- Opening Zone: Nifty opened down by 51.90 points at 24,544.25 and traded between a high of 24,585.50 and a low of 24,337.50.

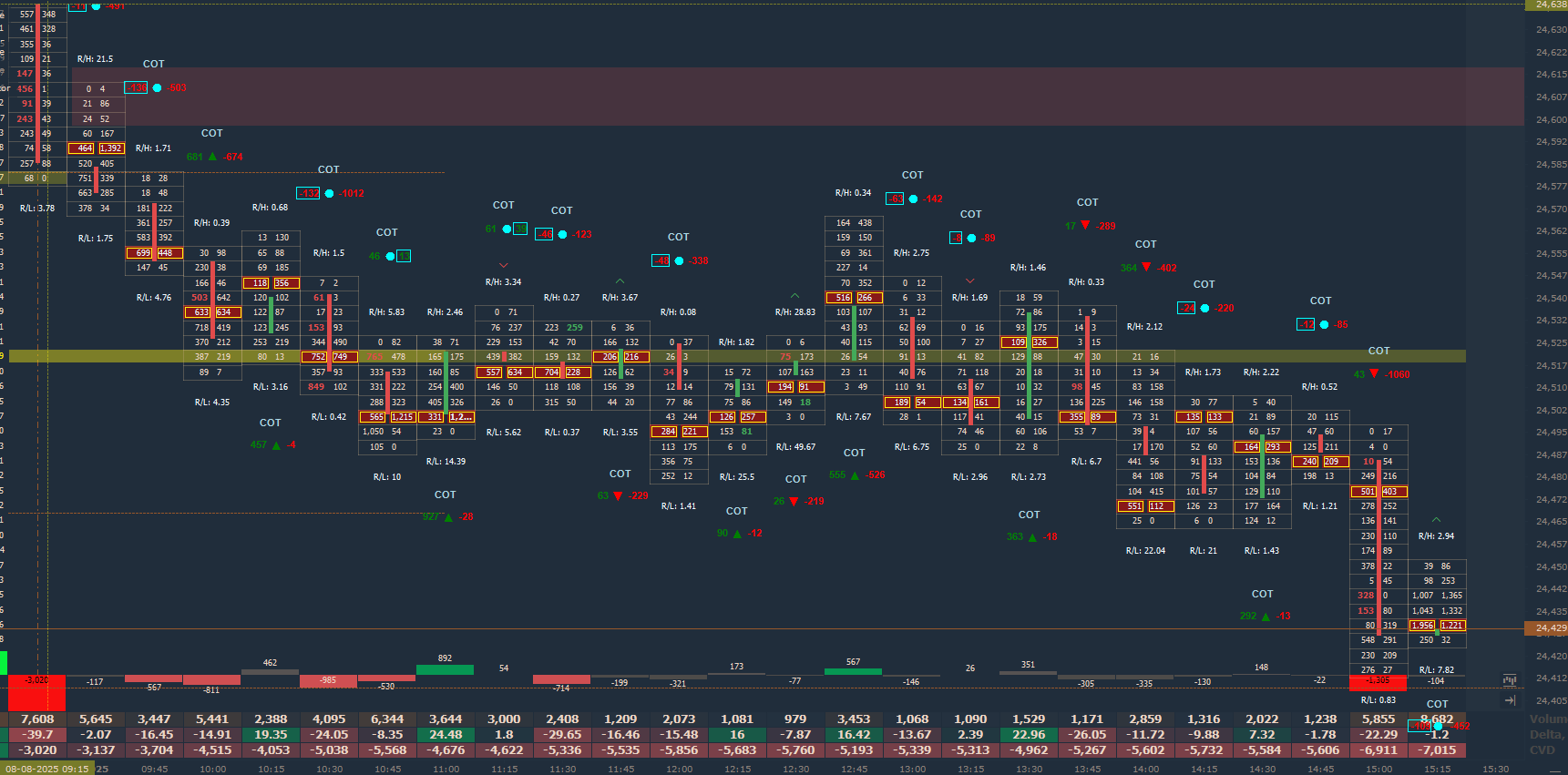

- Intraday Sentiment: The market opened negative with a heavy selling bias, reflected by a large negative delta of 727 and a negative delta % of 21.59%, signaling aggressive seller dominance throughout the session.

- Efforts to rally between 12:05 PM and 12:55 PM were short-lived, as renewed selling at 1 PM pushed markets further down, rejecting previous volume Point of Control (POC) levels observed on August 6.

- The continuous rise in cumulative negative delta meant limited opportunities for call buyers intraday, although scalpers found chances to profit on small moves.

Volatility and Market Sentiment

- The India VIX rose by 3.70%, indicating increased investor anxiety and heightened market volatility in response to persistent global uncertainties and tariff-related concerns.

- Market entered a very high-volatility zone, suggesting traders should exercise caution, reduce lot sizes, and avoid non-directional strategies that could be disrupted by sudden swings.

Open Interest and Positioning

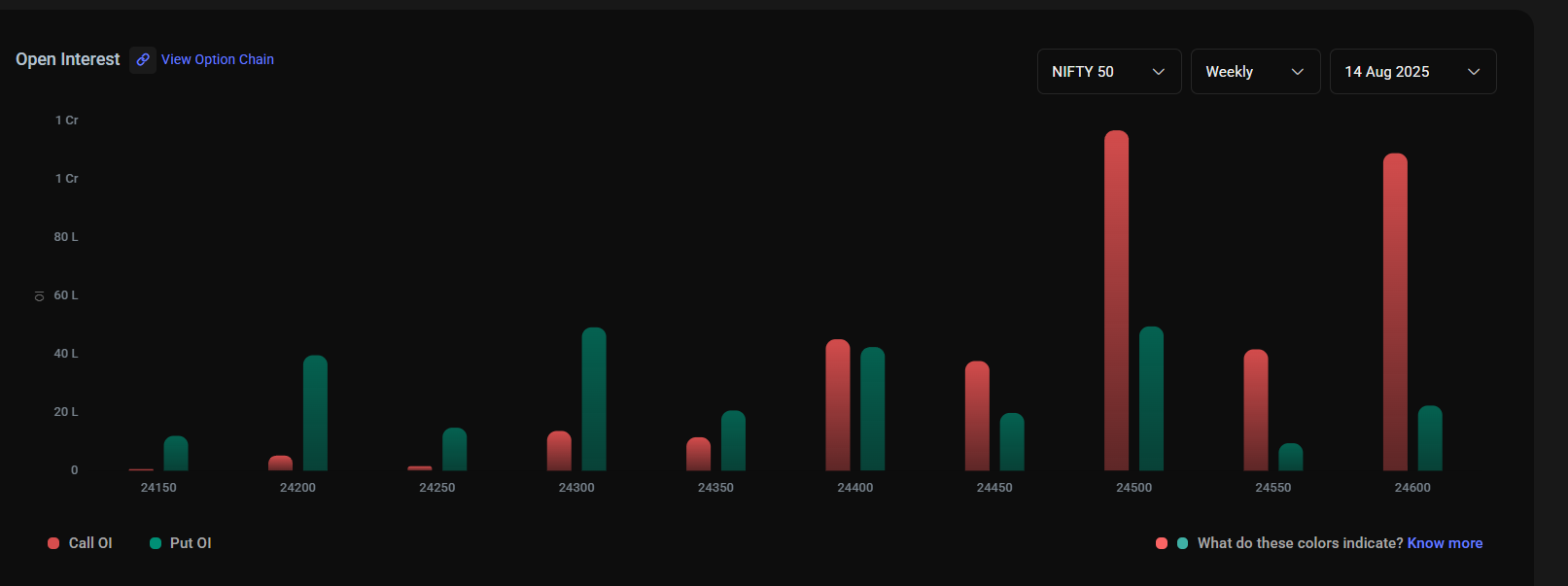

- Highest call open interest was concentrated at the 24,500 strike, likely acting as a resistance zone.

- Put open interest was not significant across strikes, while the Put-Call Ratio (PCR) stood at 0.5, reflecting a tilt towards bearish sentiment and put buying dominance.

- The session overall favored put buyers, underscoring a bearish market stance.

Sectoral Performance

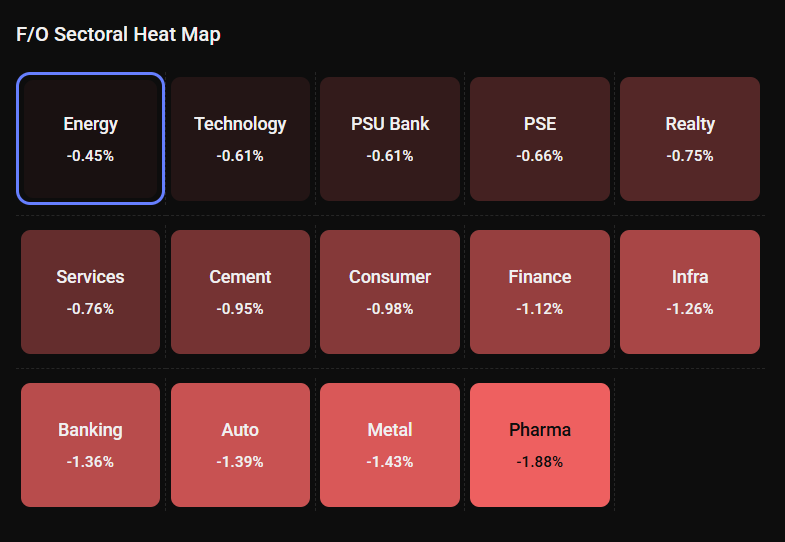

- All sectors closed in the red, with the pharmaceutical sector notably underperforming, impacted partly by tariff concerns and cautious investor stance.

Global and Domestic News Impacting the Market

- US President Donald Trump announced a 50% tariff on certain Indian goods, affecting labor-intensive export sectors such as textiles, jewellery, leather, and seafood.

- Indian textiles, jewellery, and carpet exports face severe cost hikes, risking a substantial decline in US-bound exports and putting immense pressure on MSMEs and related supply chains.

- This escalation exacerbates trade tensions and adds to foreign exchange pressure amid broader geopolitical challenges.

- India’s pharma and phone export sectors were exempted from these tariffs, but overall trade sentiment remains fragile.

Why Did Nifty Decline Today?

- The market reacted sharply to the US tariff announcement that threatens India’s key export industries, especially labor-intensive MSME-driven sectors.

- Elevated market volatility and rising India VIX reflect growing uncertainty and risk aversion.

- Persistent selling pressure from both domestic and foreign participants, reflected in negative intraday deltas and lack of significant put open interest support.

- Rejection from important volume POC levels from August 6 suggests that key technical supports failed to hold, reinforcing bearish momentum.

- Global concerns, including unresolved trade disputes and geopolitical risks, further weigh on investor confidence.

Bonus Points and Recommendations

- Given the highly volatile environment, traditional support and resistance levels are less reliable.

- Risk management is critical: reduce position sizes and avoid non-directional option strategies that could be derailed by volatility spikes.

- Scalping may provide short-term opportunities, but larger intraday directional trades warrant caution.

- Watch the 24,500 levels closely as the resistance and short-term pivot zone.

Note: This market commentary is for educational purposes only. I am not a SEBI-registered advisor. Stock markets involve risks—consult a certified financial advisor before making investment decisions. This is an independent analysis and not an endorsement of any platform or product.

Comments are closed