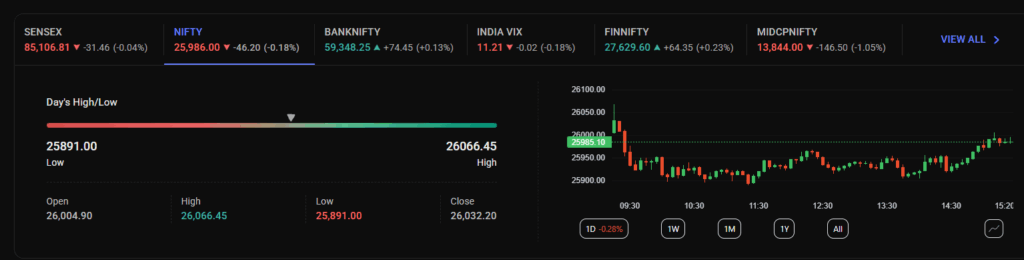

Market summary

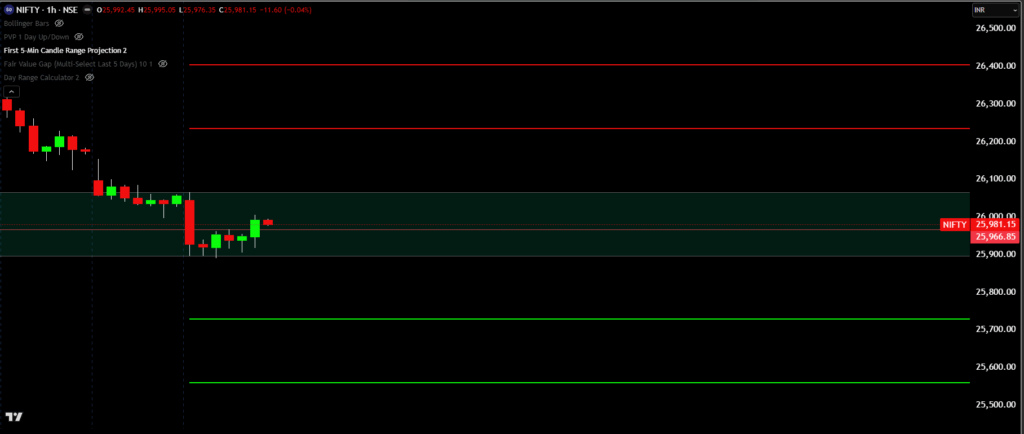

Nifty opened almost flat with a mild gap down of 27.30 points at 26,004.90 and immediately showed strong selling pressure. In the first 5 minutes, delta was around -56,325, with intraminute negative delta accelerating toward roughly -73,350 and a max negative delta around -67,5xx, clearly indicating aggressive sellers dominating on the tape. This early negative order‑flow suggested that the 26,000 zone was vulnerable, and price indeed broke below 25,900 intraday while forming a bearish FVG (fair value gap), confirming downside imbalance and lack of reliable support during the morning session.

Today’s IB range versus average range at 184/106.75 shows that the initial balance itself expanded quickly relative to the usual move, matching the theme of early directional selling. Around 11:30, the market found some short‑term support and attempted a recovery, but there were continuous call writers active at 26,100 and 26,000, which kept upside capped and sentiment weak. Only in the last hour did the index manage a better pullback—likely on profit‑booking by intraday shorts—allowing Nifty to close back near the psychological 26,000 mark instead of at the lows.

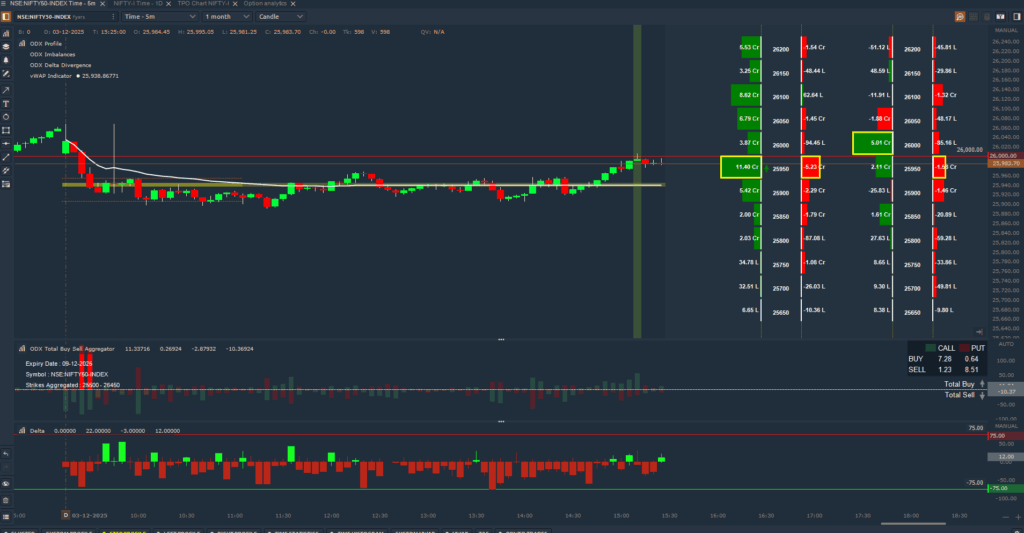

Technical points – structure and intraday stats

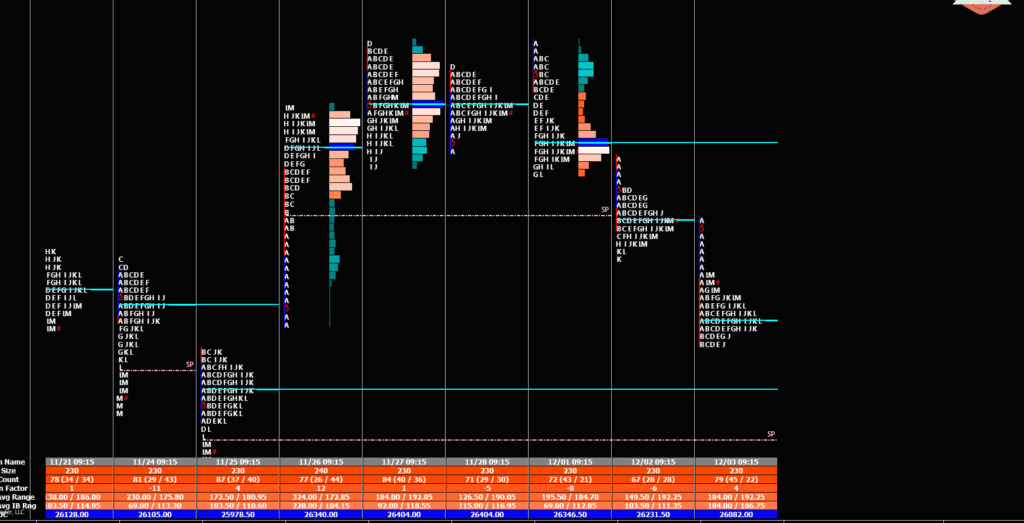

Today’s POC at 25,900 shows that maximum traded volume built up in the lower half of the day’s range, which aligns with a “value shifting down” profile and supports the view that supply was in control for most of the session. A rotation factor of -2 indicates a mildly trending‑down type day rather than a very choppy auction, while a POC count of 7 shows repeated trading and acceptance around 25,900, potentially turning it into an important intraday reference level for the coming sessions.

In price‑action terms, the break below 25,900, formation of a bearish FVG, and sustained negative delta suggest that rallies are likely to be sold into until the market can reclaim 26,000–26,050 with strength and positive delta. For tomorrow, traders should watch 25,900 as immediate intraday support and 26,000–26,100 as a supply zone dominated by call writers; failure to hold 25,900 could open room for a deeper test toward lower put‑heavy strikes into the 9 November expiry.

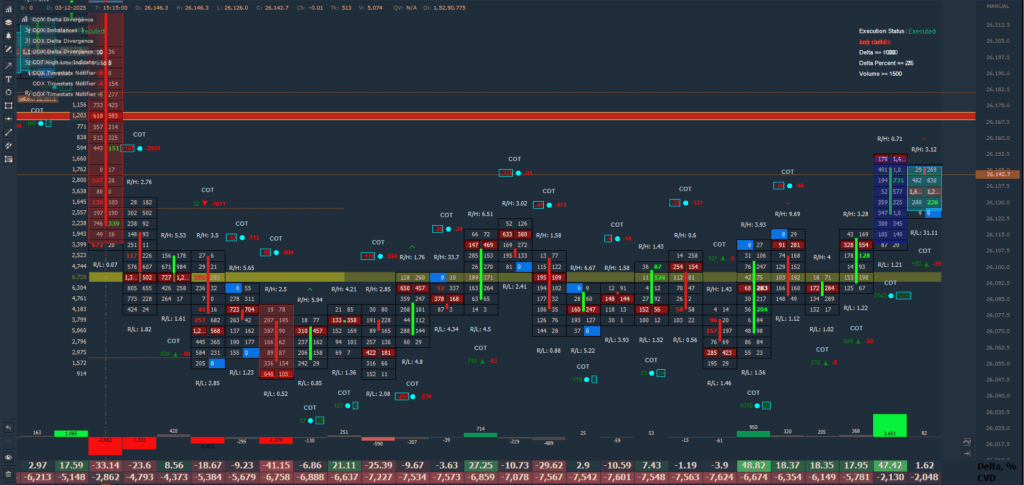

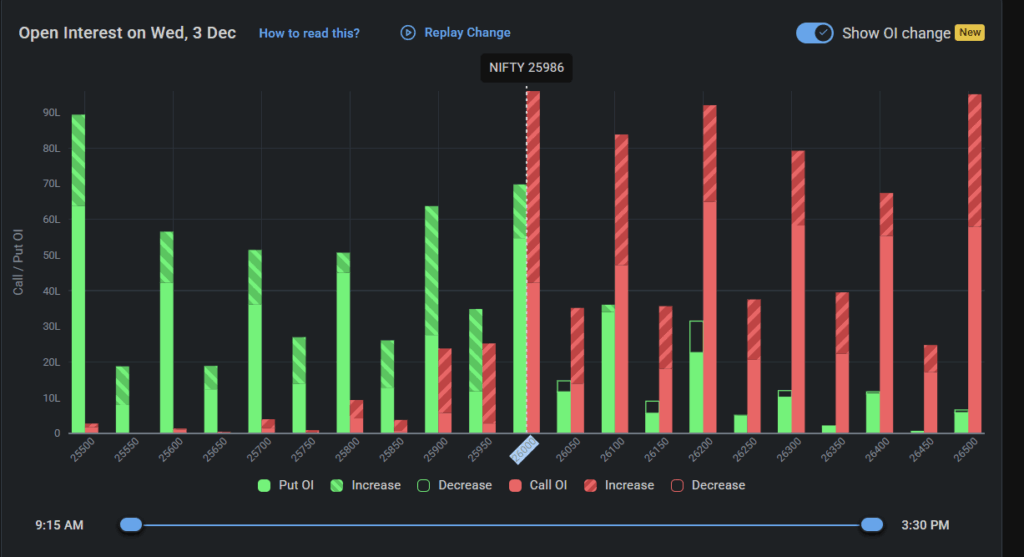

Open interest for 9 December expiry

For the 9 December expiry, call open interest is highest at 26,000, while the highest put OI sits at 25,500. This configuration creates a short‑term options range of 25,500–26,000, with 26,000 acting as a strong resistance wall and 25,500 as key downside protection where put writers are willing to absorb risk.

The highest change in OI on the 26,000 call side shows that fresh call writing is happening right at the psychological round number, signaling that many traders expect rallies towards 26,000 to be capped in the near term. On the put side, the highest OI change at 25,500 suggests that dip‑buyers or hedged writers are stepping in at lower levels, but they are not yet confident enough to shift their base higher to 26,000. Together, this reflects a market with a bearish to mildly sideways bias into expiry, where every bounce is used to sell calls closer to 26,000.

Sectoral movement

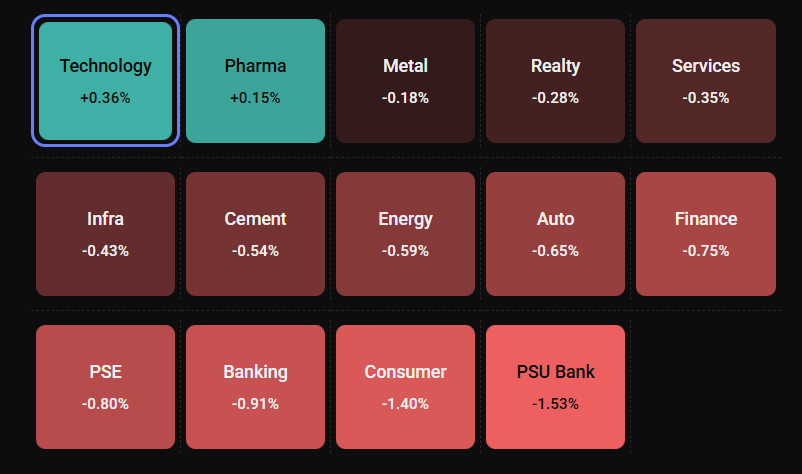

Sectorally, the market breadth was weak. Technology and pharma were the only notable gainers, benefiting from defensive interest and relative resilience, as traders rotated towards sectors that typically hold better during uncertain or corrective phases. Other sectors traded in the red, reinforcing the idea that selling pressure was broad‑based outside a few defensive and export‑oriented pockets.

This kind of sectoral pattern—defensive sectors gaining while cyclicals and broader segments correct—often appears when the market is digesting previous rallies, foreign flows are cautious, or macro headlines increase uncertainty around growth, currency, or rates.

Global news

Global and domestic macro headlines added to the cautious tone. India’s services PMI showed that services growth accelerated in November, but the export component remained weak, implying that domestic demand is healthy while external demand is under pressure. Gold holding steady ahead of key US data underscores that global markets are still watching interest‑rate expectations and risk‑off hedging behavior closely.

The note that the Indian rupee risks a steeper fall past 90 without central bank support highlights currency‑related worries. A weaker rupee can hurt imported inflation, corporate margins dependent on imports, and foreign investor confidence, which in turn can weigh on equities even if headline volatility (VIX) stays low. These factors help explain why Nifty faced selling pressure despite no major spike in volatility.

Bonus point – trading and risk management

Your guidance to trade with small capital and proper hedges in a volatile environment is very apt. Even though VIX is near 11, intraday ranges, delta swings and gap openings show that real trading risk is still high, especially around key levels like 26,000 that are crowded with option writers. Until macro uncertainties around currency, exports and global rates calm down, it makes sense to preserve capital by sizing down, using spreads and defined‑risk strategies, and avoiding emotional over‑trading.

Once conditions stabilise, liquidity normalises and option prices better reflect realized volatility, positions can be scaled back up with clearer trend confirmation instead of fighting choppy moves.

Educational and disclaimer note

This blog is purely for educational purposes and is not SEBI‑registered investment advice. Securities markets are risky; always consult a qualified financial advisor before investing or trading. You are not associated with any broker or trading platform; images or P&L shared are only to remove negativity about options and to show that options, when used correctly, are tools for risk management, not guaranteed profit machines. You are not selling any course or product, just sharing personal views and trades that may be wrong—readers should treat this as learning content only.

Comments are closed